Affordability plays a decisive role of in achieving universal and meaningful connectivity (UMC); digital poverty leads to exclusion from essential digital opportunities. High costs for both ICT services and devices are commonly cited barriers to Internet use, particularly among low-income households.

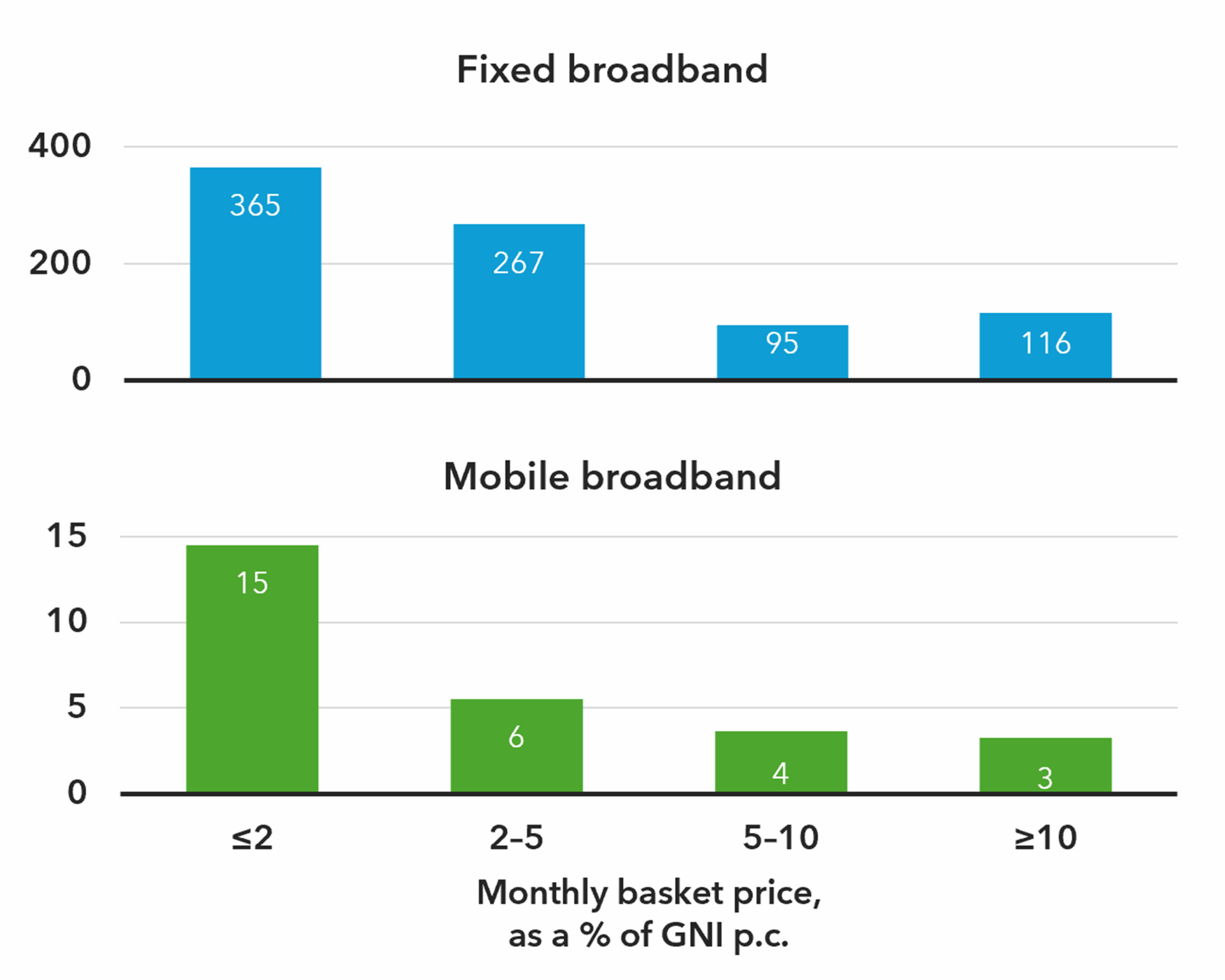

Data shows a negative correlation between Internet use and price. In economies where the price of mobile broadband amounts to a significant share of the monthly Gross National Income (GNI) per capita, not only is the share of Internet users lower, but the data usage per subscription is also more limited than elsewhere. By contrast, economies meeting the Broadband Commission’s aspirational target (entry-level broadband services costing less than 2 per cent of monthly GNI per capita) have the highest shares of Internet users in the population, and experience significantly higher data traffic.

Monthly Internet data traffic per subscription in GB, by basket price ranges, 2025

Notes: median monthly traffic per subscription, by affordability ranges.

Source: ITU

Households differ considerably in terms of expenditure on ICT services, and there are considerable gaps both between countries as well as within countries. In the richest countries, ICT services account for 2–3 per cent of household expenditure, while in lower-income economies, this share varies widely, ranging up to nearly 9 per cent. Rural populations often spend a higher share of their income for connectivity than urban populations, typically receiving lower-quality services due to higher deployment costs outside urban areas.

Global trends show marked improvement in affordability between 2013 and 2025: the median price level of entry-level mobile broadband dropped by about 50 per cent (in PPP USD, adjusted for inflation), and affordability as a share of GNI per capita improved by approximately 40 per cent, reaching 1.4 per cent globally.

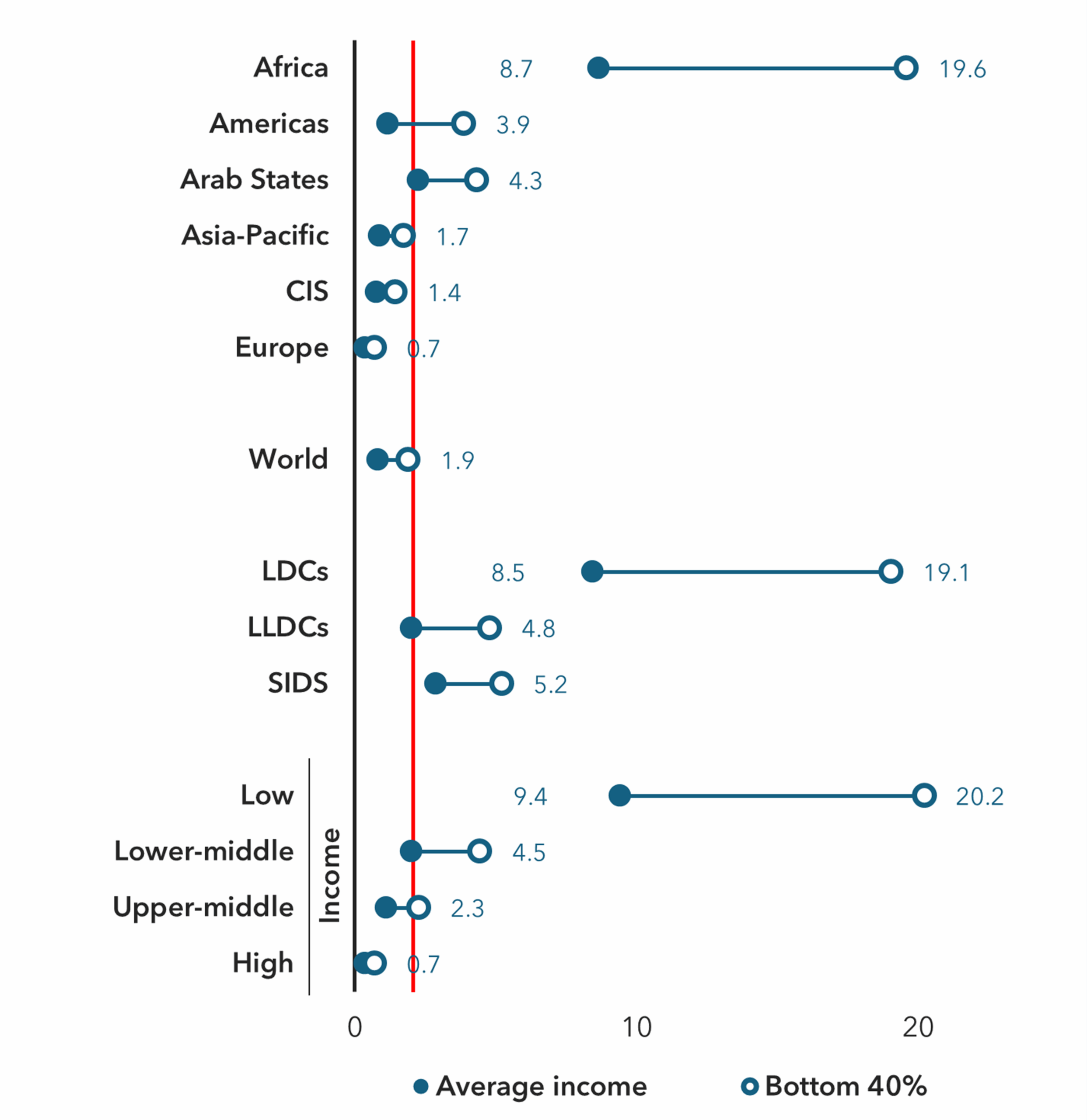

Despite these gains, major affordability divides persist between income groups. In low-income economies, in nine out of ten countries, a 5 GB mobile broadband basket costs more than 10 per cent of the average monthly income, far exceeding the 2 per cent target.

Crucially, affordability gaps within countries are severe for the lowest earners. For the bottom 40 per cent of earners in Least Developed Countries (LDCs) and low-income economies, the cost burden rises to about 20 per cent of their GNI per capita, effectively doubling the affordability challenge compared to the national average.

Mobile broadband affordability gaps between the bottom 40% and average income (% of GNI per capita), 2025

Note: based on 107 countries with available recent inequality survey data (not older than 2019) and price data (2025).

Source: World Bank PIP, ITU

Cross-country price differences stem from structural factors, policy choices, and market dynamics. Structural challenges include high network deployment costs in countries with challenging geographies and unfavourable macroeconomic conditions. A key external driver of high costs in regions like Sub-Saharan Africa is the weakness of electricity infrastructure; reliance on diesel generators significantly raises operating costs.

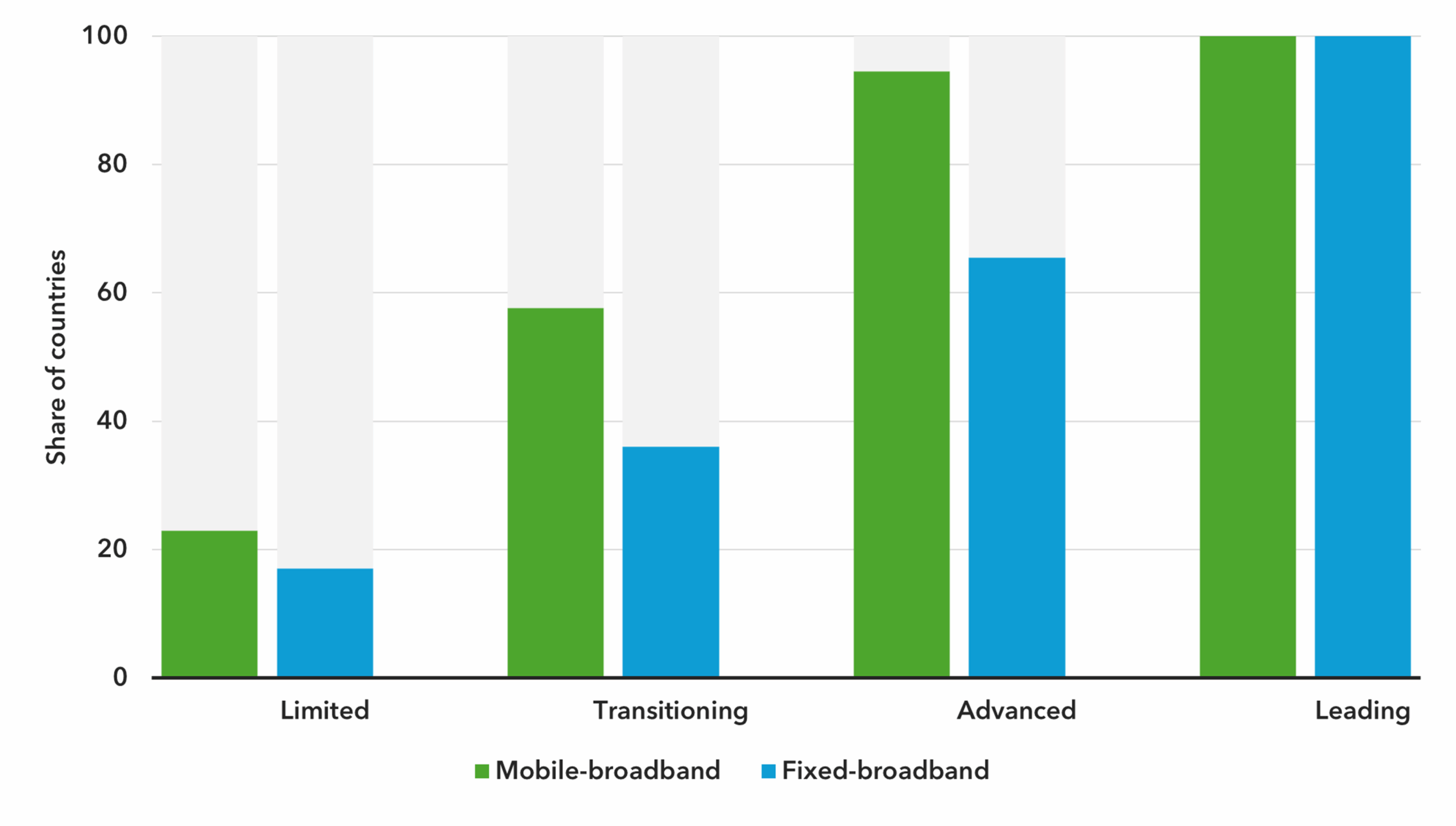

Policy levers are essential to improving affordability. The degree of competition in the telecommunication market is a critical driver, with higher competition generally leading to lower consumer prices. Furthermore, a coherent digital regulatory framework is paramount. Broadband services tend to be more affordable in countries where digital governance mechanisms are mature and well-established.

Share of economies where ICT services are affordable (up to 2% of GNI per capita), by maturity of national enabling environment for digital markets (G5 Benchmark)

Sources: ITU; ITU G5 Benchmark (2023)

Closing the affordability gap requires continued monitoring, comprehensive policies addressing supply and demand sides, enhanced competition, and targeted efforts addressing potential inter-regional affordability divides within countries as well as focusing on the lowest-income populations.