Page 614 - AI for Good Innovate for Impact

P. 614

AI for Good Innovate for Impact

Integrated statistical tests (e.g., demographic parity, disparate impact ratio) to ensure threshold

updates do not introduce or exacerbate bias, with regular reporting to regulators.

• REQ-08: Visualization Dashboard

Interactive dashboard (e.g., within Google Colab or web User Interface(UI)) displaying current

values of threshold levels, profit curves, feature importances, and MCMC trace plots for

stakeholder validation.

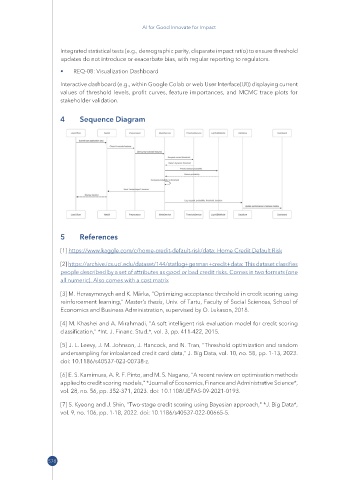

4 Sequence Diagram

5 References

[1] https:// www .kaggle .com/ c/ home -credit -default -risk/ data: Home Credit Default Risk

[2] https:// archive .ics .uci .edu/ dataset/ 144/ statlog+ german+ credit+ data: This dataset classifies

people described by a set of attributes as good or bad credit risks. Comes in two formats (one

all numeric). Also comes with a cost matrix

[3] M. Herasymovych and K. Märka, "Optimizing acceptance threshold in credit scoring using

reinforcement learning," Master’s thesis, Univ. of Tartu, Faculty of Social Sciences, School of

Economics and Business Administration, supervised by O. Lukason, 2018.

[4] M. Khashei and A. Mirahmadi, "A soft intelligent risk evaluation model for credit scoring

classification," *Int. J. Financ. Stud.*, vol. 3, pp. 411-422, 2015.

[5] J. L. Leevy, J. M. Johnson, J. Hancock, and N. Tran, "Threshold optimization and random

undersampling for imbalanced credit card data," J. Big Data, vol. 10, no. 58, pp. 1-13, 2023.

doi: 10.1186/s40537-023-00738-z.

[6] E. S. Kamimura, A. R. F. Pinto, and M. S. Nagano, "A recent review on optimisation methods

applied to credit scoring models," *Journal of Economics, Finance and Administrative Science*,

vol. 28, no. 56, pp. 352-371, 2023. doi: 10.1108/JEFAS-09-2021-0193.

[7] S. Kyeong and J. Shin, "Two-stage credit scoring using Bayesian approach," *J. Big Data*,

vol. 9, no. 106, pp. 1-18, 2022. doi: 10.1186/s40537-022-00665-5.

578