Page 271 - The Digital Financial Services (DFS) Ecosystem

P. 271

ITU-T Focus Group Digital Financial Services

Ecosystem

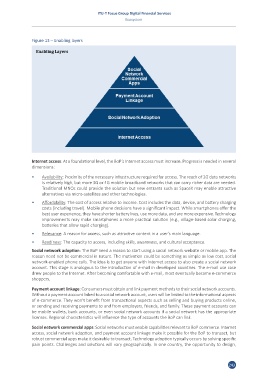

Figure 13 – Enabling layers

Internet access: At a foundational level, the BoP’s Internet access must increase. Progress is needed in several

dimensions:

• Availability: Proximity of the necessary infrastructure required for access. The reach of 2G data networks

is relatively high, but more 3G or 4G mobile broadband networks that can carry richer data are needed.

Traditional MNOs could provide the solution but new entrants such as SpaceX may enable attractive

alternatives via micro-satellites and other technologies.

• Affordability: The cost of access relative to income. Cost includes the data, device, and battery charging

costs (including travel). Mobile phone decisions have a significant impact. While smartphones offer the

best user experience, they have shorter battery lives, use more data, and are more expensive. Technology

improvements may make smartphones a more practical solution (e.g., village-based solar charging,

batteries that allow rapid charging).

• Relevance: A reason for access, such as attractive content in a user’s main language.

• Readiness: The capacity to access, including skills, awareness, and cultural acceptance.

Social network adoption: The BoP need a reason to start using a social network website or mobile app. The

reason need not be commercial in nature. The motivation could be something as simple as low cost, social

network-enabled phone calls. The idea is to get anyone with Internet access to also create a social network

account. This stage is analogous to the introduction of e-mail in developed countries. The e-mail use case

drew people to the Internet. After becoming comfortable with e-mail, most eventually became e-commerce

shoppers.

Payment account linkage: Consumers must obtain and link payment methods to their social network accounts.

Without a payment account linked to a social network account, users will be limited to the informational aspects

of e-commerce. They won’t benefit from transactional aspects such as selling and buying products online,

or sending and receiving payments to and from employers, friends, and family. These payment accounts can

be mobile wallets, bank accounts, or even social network accounts if a social network has the appropriate

licenses. Regional characteristics will influence the type of accounts the BoP can link.

Social network commercial apps: Social networks must enable capabilities relevant to BoP commerce. Internet

access, social network adoption, and payment account linkage make it possible for the BoP to transact, but

robust commercial apps make it desirable to transact. Technology adoption typically occurs by solving specific

pain points. Challenges and solutions will vary geographically. In one country, the opportunity to design,

243