The satellite industry since WRC-2000

|

ITU 030029/Euroconsult

|

The satellite industry continues to experience growth in spite of set-backs

in the development of Global Mobile Personal Communication Services by

Satellite. For some time now, the demand for spectrum/orbit usage has been

increasing for virtually all space communication services but most notably

for fixed-satellite, broadcasting-satellite and mobile-satellite services.

Market research* on satellite business estimates that between 175 and 201

satellites will be launched over the period 20012010 to meet demand, with a

market value of USD 21.926.5 billion. However, in the period since the World

Radiocommunication Conference in 2000 (WRC-2000), the general economic

conditions and the mixed fortunes of telecommunication carriers and the industry

as a whole have been very visible in satellite services development.

Fixed-satellite services

The year 2002 is said to have marked the second year of negative growth in

revenues for FSS operators. With consolidated revenue estimated at USD 6.6

billion in 2002, the 36 FSS satellite operators (see Table 1) are said to have

experienced a year of negative growth (4.4 per cent). This contrasts with the

record growth achieved in 2000 when revenue topped USD 7 billion. While the year

2000 was boosted by exceptional events, in 2001 and 2002 the industry had to

cope with the fall of the telecommunications market. Despite the decline in

revenues, the FSS industry is expected to remain healthy, with possible recovery

in 2003.

The world availability of satellite transponders is reported to have grown

strongly in 2002, with 950 new transponders available on 20 newly launched

satellites, contrasting with only 400 new transponders on 10 satellites in 2001.

In Russia, for example, two domestic satellite operators, RSCC and Gascom, are

in the process of renewing and enlarging their fleets. In 2000, RSCC decided to

launch a new series of six Express satellites, which will expand its fleet

from 95 to around 250 transponders. While the majority of this capacity will be

used by Russian customers, the excess will be sold to customers in Asia,

especially in China. Gascom, related to gas company Gazprom, has two more Yamal

satellites under construction. Gazprom is a major customer of Gascom, utilizing

around 40 per cent of the satellite transponder capacity. Other customers

include Russian network television, government and telecommunication companies.

Much of RSCCs capacity is used for VSAT networks.

| * Conducted by Euroconsult, a Paris-based leading consulting company

on satellite business (www.euroconsult-ec.com).

The market research and analysis outlined in this article is based on

Euroconsult data, unless otherwise indicated.

|

|

|

_

|

|

|

Table 1 The 36 fixed-satellite service (FSS)

operators

|

|

| |

Operator

|

Satellite system

|

Service coverage |

|

|

Trans-oceanic |

Continental |

| |

APT Satellite |

Apstar |

|

|

|

|

ASCO |

Arabsat |

|

|

|

| |

Asia Satellite |

Asiasat |

|

|

|

|

Binariang |

Measat |

|

|

|

| |

China Satcom |

Chinastar, Chinasat |

|

|

|

|

Egyptian Satellite |

Nilesat |

|

|

|

| |

Eurasiasat |

Eurasiasat |

|

|

|

|

EuropeStar |

EuropeStar |

|

|

|

| |

Eutelsat |

Eutelsat 2, Hot Bird, W, Seasat |

|

|

|

|

France Telecom |

Telecom 2 |

|

|

|

| |

Gascom |

Yamal |

|

|

|

|

Hispasat |

Hispasat |

|

|

|

| |

Insat |

Insat |

|

|

|

|

Intelsat |

Intelsat |

|

|

|

| |

JSAT |

JCSat, Nstar |

|

|

|

|

Korea Telecom |

Koreasat |

|

|

|

| |

Loral Skynet |

Telstar |

|

|

|

|

Mabuhay |

Agila |

|

|

|

| |

Nahuelsat |

Nahuel |

|

|

|

|

New Skies Satellites |

NSS |

|

|

|

| |

NSAB |

Sirius |

|

|

|

|

RSCC |

Gorizont, Express |

|

|

|

| |

Satelindo |

Palapa |

|

|

|

|

Satelites Mexicanos |

Satmex, Solidaridad |

|

|

|

| |

SES Global |

Astra, AMC |

|

|

|

|

Shin Satellite |

Thaicom |

|

|

|

| |

SingTel Optus |

ST, Optus |

|

|

|

|

Sino Satellite |

Sinosat |

|

|

|

| |

SCC |

Superbird |

|

|

|

|

Spacecom |

Amos |

|

|

|

| |

Star One |

Brazilsat |

|

|

|

|

Telkom Indonesia |

Telkom |

|

|

|

| |

PanAmSat |

Galaxy, PAS |

|

|

|

|

Telenor |

Thor |

|

|

|

| |

Telesat Canada |

Anik, Nimiq |

|

|

|

|

Turk Telekom |

Turksat |

|

|

|

| |

©

Sourced from Euroconsult 2003. |

Mobile telephony: still a niche market for satellite

While mobile-satellite services (MSS) have experienced difficult times in

recent years, in 2002 the MSS operators continued to make progress, but with

very different business models. For example, Inmarsat, signed up its 250 000

customers and launched its interim high-speed (144 kbit/s) service ahead of the

launch of BGAN in 2004, which is expected to provide a mobile 400 kbit/s

service. Iridium Satellite, which rose from the bankruptcy of Iridium LLC,

renewed its contract with a partner, securing its future at least for the near

term. The regional MSS operators, ACeS in Asia and Thuraya in the Middle East

are reassessing their business models. ACeS, while not abandoning the mobile

service, is looking to use its capacity to provide fixed rural telephony where

demand is high and unmet.

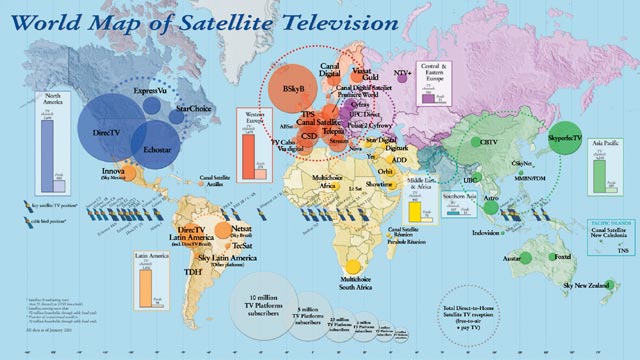

Satellite television broadcasting

Growth continues in revenues, television channels and subscribers

With an estimated 50 per cent of the transponders in orbit broadcasting

television channels, broadcasters remain the largest customers for the FSS

industry, providing over 60 per cent of its revenues.

Despite a difficult economy, the direct-to-home (DTH) satellite television

broadcasting industry continued to grow in 2002. Market research shows that some

six million additional television households subscribed to satellite pay-TV

during 2002, bringing the total of satellite television subscribers to over 52

million households at year-end. The top three satellite broadcasters were

Echostar (1.3 million net new subscribers) and DirecTV (1 million new

subscribers) in the United States, and BSkyB in the United Kingdom (800 000 new

subscribers). During the same year, SkyPerfecTV in Japan passed the 3-million

subscriber mark (400 000 new subscribers) and Canal Satellite in France the

2-million mark (150 000 new subscribers). Revenues of satellite pay-TV increased

from USD 22 billion in 2001 to around 25.5 billion in 2002 for the 55 DTH

multi-channel pay-TV broadcasters.

According to industry forecasts, the cable and satellite industry in Asia and

the Pacific is set to grow from the current 157 million subscribers to over 228

million in the next eight years, recording a 45 per cent growth rate from 2002

to 2010. China and India are expected to continue to be the key markets in 2010,

with 128 million subscribers in China and 53.35 million in India. ** According to industry forecasts, the cable and satellite industry in Asia and

the Pacific is set to grow from the current 157 million subscribers to over 228

million in the next eight years, recording a 45 per cent growth rate from 2002

to 2010. China and India are expected to continue to be the key markets in 2010,

with 128 million subscribers in China and 53.35 million in India. **

Satellite television channels

Some 1150 new satellite television channels were launched worldwide in 2002,

bringing the net total to about 10 500 channels currently broadcast by

satellite. In a difficult advertising market, growth was largely sustained by

multi-channel pay-TV offerings with about 750 new television channels broadcast,

and a further 400 new free-to-air and individual premium channels. Growth is

expected to continue in 2003 with good medium-term prospects sustained by

consolidation in the DTH satellite broadcasting industry.

|

ITU 030004/PhotoDisc

|

Further developments to be considered at WRC-03

Radio frequencies and the geostationary satellite orbit are limited natural

resources, which must be used rationally, efficiently and economically. The

International Telecommunication Union (ITU) upholds the right of all countries

to equitable access to satellite orbit space. International agreement on the way

the various bands of the radio-frequency spectrum are used is essential to the

smooth operation of a growing range of critical applications, from aircraft and

maritime navigation to wireless telephony, satellite broadcasting and scientific

research. On this score, the ITU Radiocommunication Sector (ITUR) and in

particular world radiocommunication conferences play a vital role in regularly

updating the basis for allocation and use of the radio-frequency spectrum and

satellite orbits.

|

ITU 030032/PhotoDisc

|

Spectrum allocation and sharing will be a challenge for the upcoming World

Radiocommunication Conference (WRC-03), to be held in Geneva from 9 June to 4

July 2003. WRC is the forum that defines and updates the Radio Regulations

the binding international treaty that governs the allocation and use of the

radio-frequency spectrum by a plethora of different services worldwide.

|

ITU

010101/PhotoDisc

|

Private sector plans to deploy new non- geostationary satellite

constellations to deliver voice telephony and broadband data services, along

with a new wave of traditional geostationary satellite deployments geared

to meeting steadily rising demand for Pay-TV, future interactive entertainment

services, high-speed Internet and corporate networking, all necessitate the

development of technical sharing criteria and arrangements to ensure that

neither type of satellite system would cause harmful interference to the smooth

functioning of the other. Such ongoing developments have required detailed

consideration of new or revised technical solutions. For example, additional

spectrum allocations made by WRC-97 to planned non-geostationary fixed-satellite

systems (NGSO FSS) were subject to strict power limits in order to protect GSO

and other services already operating in those bands.

WRC-03 will be key in updating the regulatory framework, as well as the

sharing scenarios and methodologies in order to ensure a fair and efficient use

of the radio-frequency spectrum to enable the various industry segments to

deploy new services or expand existing ones to generate capacity for new

services and technologies. In this regard, the work carried out by ITUR study

groups, the Special Committee on Regulatory and Procedural Matters and the

Conference Preparatory Committee in preparation for WRC-03 makes possible the

necessary technical and operational bases on which to take sound decisions.

|

** Based on the latest figures published by the Cable and Satellite

Broadcasting Association of Asia (CASBAA).

|

|